Topic 3: MARKET SNIPPETS

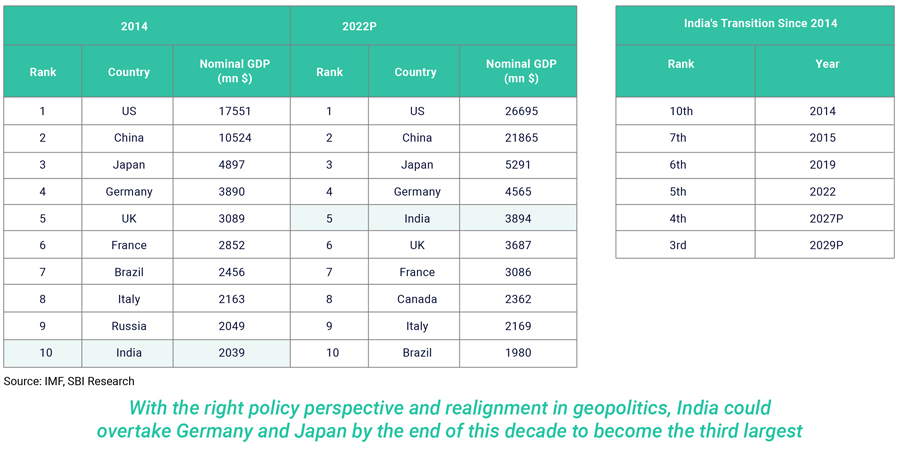

India overtakes the UK to become the 5th largest economy in the world

Top 10 Economies, Nominal GDP ($ mn)

Moody’s affirms stable outlook for India

Moody’s retained India’s sovereign credit rating at Baa3 with a stable outlook citing that India’s credit profile reflects high growth potential, strong external

position, and a stable domestic financing base for government debt. Also, the rating agency does not expect global challenges including the impact of the

Russia-Ukraine conflict, higher inflation, and tightening global financial conditions to derail India’s economic recovery from the pandemic.

Moody’s highlighted that India could see a rating upgrade if the growth potential increases materially beyond their expectations, supported by effective

policy implementations that could lead to a significant and sustained pickup in private sector investment. However, factors like weaker economic growth or

a resurgence of financial sector risk could put downward pressure on the ratings.

JP Morgan likely to include India in its emerging market bond index

Indian bonds are poised to rally as JPMorgan is likely to include India in its widely tracked emerging-market bond index, setting the stage for billions of

dollars of inflows. The index team has more incentive to include India on the back of Russia’s exclusion and most investors either support or have no

objection. However, the timeline for the announcement of inclusion is yet unknown. The massive inflow over the next one-year will support the G-sec bond

yields and help strengthen INR

ECB hikes interest rate by another 75 bps

After raising interest rates for the first time in over a decade at their last meeting, European Central Bank (ECB) policymakers deliver another bumper hike to fight

against soaring inflation. The ECB is catching up as far as rate hikes are concerned, and this hike sends a clear message about ECB’s intention to tame inflation.

Steep increases in energy prices in the wake of the Russian invasion of Ukraine have heaped pressure on households and sent Eurozone inflation to new highs.

The recent halt of gas deliveries to Europe via the Nord Stream 1 pipeline has not only pushed stocks lower and increased the risk of a recession in Europe, but it

has also pushed bond yields higher.

The Eurozone is almost certainly entering a recession, with recent surveys showing a deepening cost of living crisis and a gloomy outlook that is keeping

consumers wary of spending. Also, some of the energy-intensive industries in Europe have already scaled back production.