As the West imposes further sanctions on Russian entities and individuals,

India continues to hold a neutral stance.

India imports nearly 80% of its fuel needs. A $5 increase in oil price

increases India’s current account deficit by $6.6 bn. Amid the rising crude

oil prices, India imports oil from Russia at a discounted price. While this

deal eases some pressure on India’s deficit situation, it invites scrutiny

from the West. Also, Russia accounts for two-thirds of India’s defence

imports

The U.S. is India’s top trading partner and the second-biggest source of

foreign direct investment. Similarly, the European Union is also a major

trade and investment partner. Any deterioration in economic ties or

sanctions, as a consequence of India’s stance, could have significant

consequences for the economy.

This places India in a tight economic and diplomatic situation. A fall to

either side could be costly.

While new threats are rising, the story of the dollar's demise as the global

reserve is highly exaggerated.

As a global reserve currency, the dollar's share has been fairly stable at

around 60%. Despite the Chinese government's efforts to trade in its own

currency in recent years, Renminbi has barely cracked 2% of the global

reserve currency.

However, there are several new and emerging threats to dollar dominance:

1. The US Fed money printing during the pandemic could lead to inflation

and a decline in the dollar

2. Rise of Cryptocurrencies, particularly Bitcoin, as an alternative to Fiat

currencies

3. Moves by Central Banks to create their own digital currencies, such as

Digital Dollar, Digital Yuan, and Digital Rupee

4. Deglobalization trend

5. Use of the dollar as a political weapon by banning Russia from using its

own dollar reserves

We believe that the percentage of global trade conducted in dollars will

decline slowly in the coming decades. However, we do not expect a steep

decline as no clear alternative is on the horizon. As long as the US

economy stays dominant, so will the dollar. However, one real risk

emerges from cryptocurrencies for Fiat currencies.

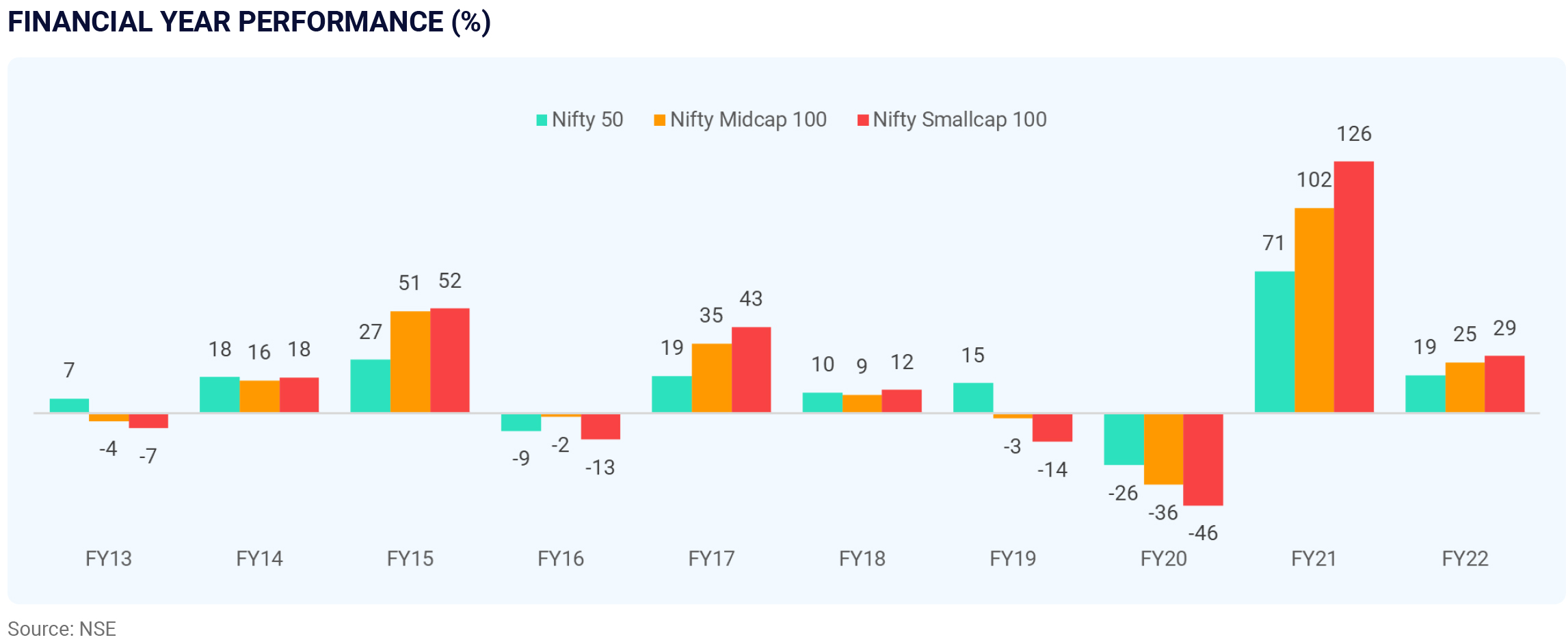

After a strong equity markets rally in FY21, the momentum continued, with the markets (as represented by Nifty 50 Index) surging another 19% in FY22. Both Nifty Midcap 100 (+25% YoY) and Nifty Smallcap 100 (+29% YoY) outperformed the large-cap segment. The positive sentiment continued for most of the year, led by a strong economic and earnings recovery. However, markets lost their sheen in the last quarter as Russia’s invasion of Ukraine destabilized the growth outlook, concerns of rising inflation, and heightened geopolitical risks.

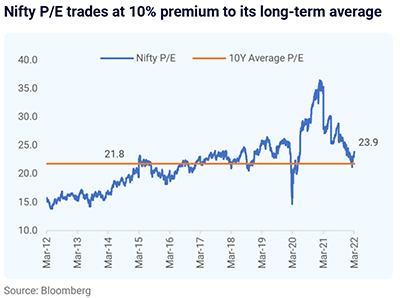

From a valuation perspective, market trades at a trailing PE (price to earnings) of 23.9x, a premium of 9.7% compared to its historical average of 21.8x.

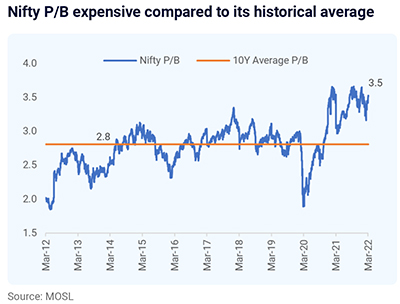

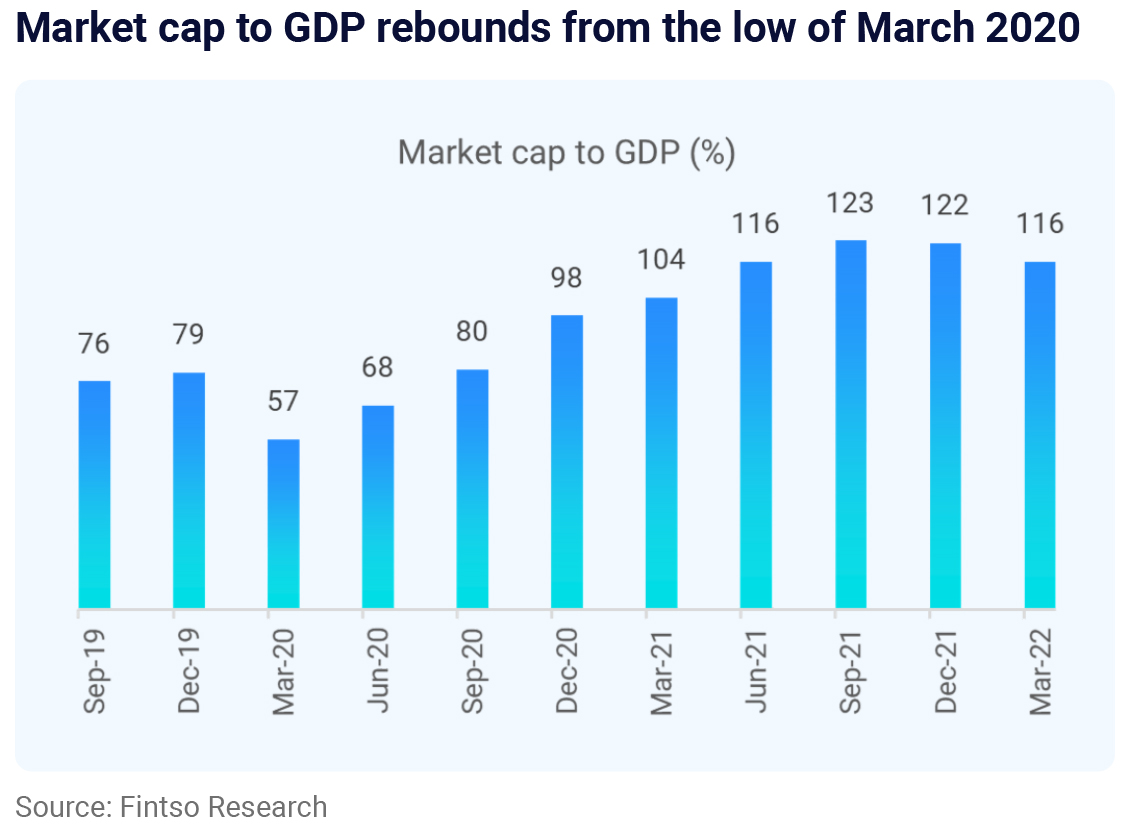

Also, PB (price to book) at 3.5x is at a 25.5% premium to its historical average. After touching a bottom of 56% in March 2020, the market capitalization to

GDP has rebounded to 116% (based on the latest GDP data available).

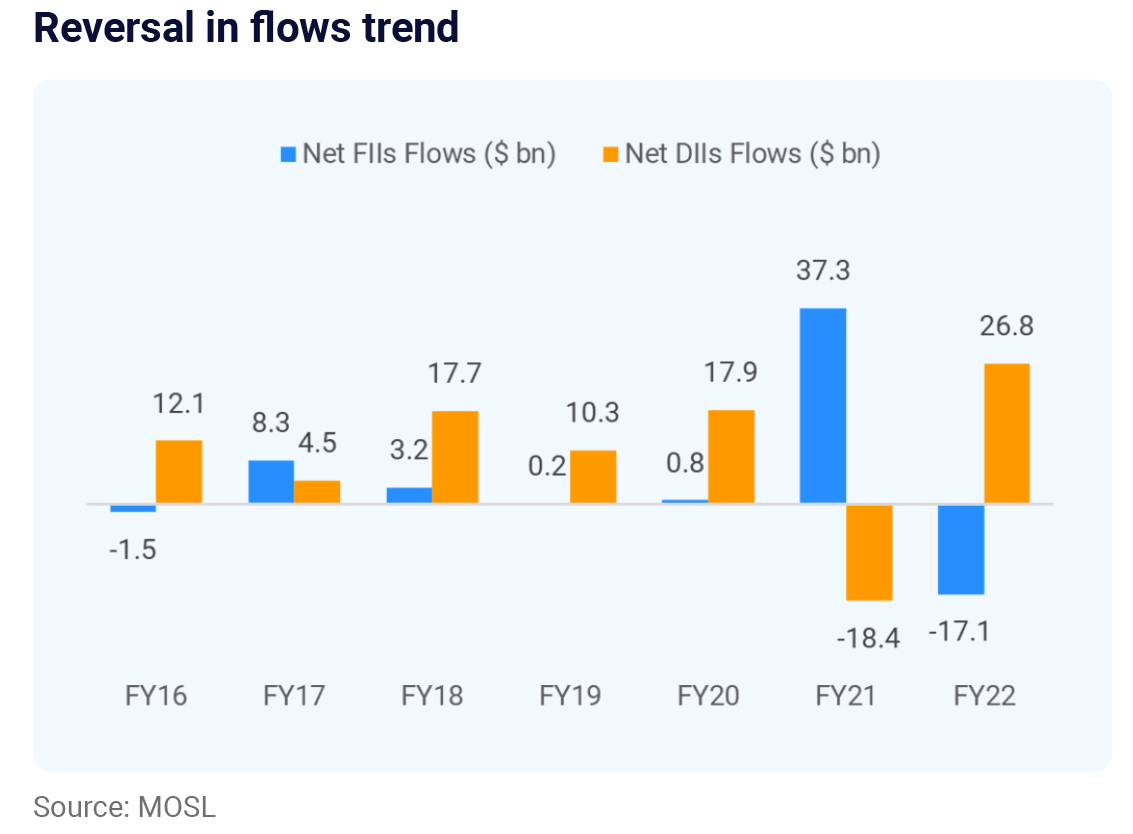

During the financial year, we witnessed a reversal in the flow trend. DIIs who have been net sellers in the last financial year turned out to be strong buyers

with record inflows at $26.6 bn, and FIIs turned net sellers after being net buyers last year.

As we step into the next financial year, we believe volatility will persist as some of the major central banks accelerate towards higher policy rates and

corporate margins start to get impacted due to rising inflation. As margins get impacted, companies shall pass on the higher prices to consumers, forcing

them to reduce discretionary spending. Also, China’s Covid-19 situation further augments the risk to the markets. The combination of input cost pressure

and slowing growth could lead to erratic earnings for FY23, especially for consumer-facing businesses. However, export-oriented businesses could benefit

from currency depreciation.

Given the headwinds for the market, we advise investors to consider staggering investments in equities through SIP or STPs. Also, if there is any major

market correction, we would recommend buying such DIPs as we believe that India has sustainable drivers for secular growth and continue to remain

bullish on equities from a long-term point of view.

To further reduce the risk, we recommend investing in 2-3 ELSS schemes. Based on our fund selection process that considers performance and fund management aspects, below is the list of our recommended ELSS schemes.

FIXED INCOME: ERA OF RISING INTEREST RATES

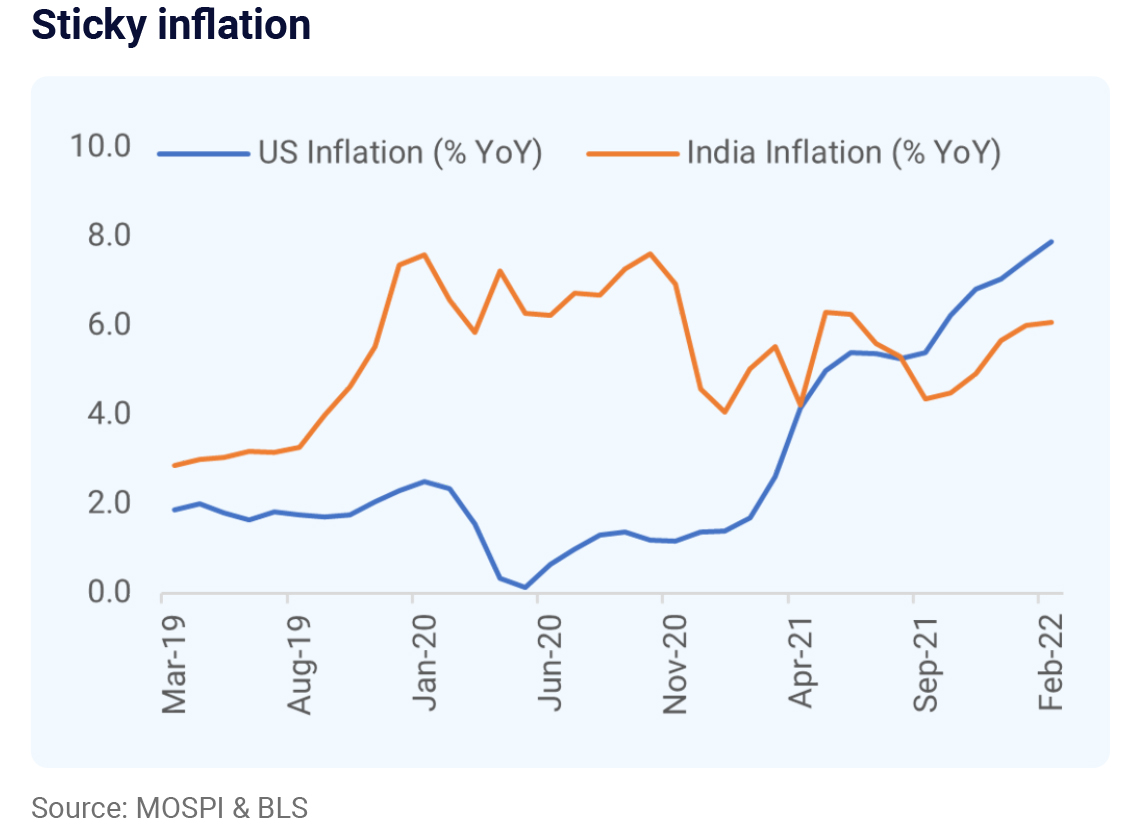

Interest rates in India and globally are expected to rise as retail inflation continues to remain elevated. While the RBI has maintained an accommodative

stance in its recent monetary policy, it would be difficult for them to continue to maintain this stance given the stickiness in the inflation rate. This would

put the RBI behind the curve in tackling inflation at a time when central banks across the globe are tightening policy to ease inflation pressure.

Also, the recent inversion of the US treasury yield curve resurfaces the risk of the global economy entering a recession. Also, Dow Jones Transportation

Average slipped into the bear market territory, another sign of bad news in store for the economy. Dow Jon Transportation Average tracks companies from

airlines, railroads, and trucking, which helps in gauging the health of the economy.

As we expect interest rates to be volatile, it is best to avoid funds investing in long-dated securities. Thereby, investors can consider investing in securities

with shorter maturity (short duration funds and banking & PSU funds). Also, one can consider investing in floater rate funds as returns are adjusted based

on prevailing yields in the market. Also, investors can look at target maturity funds if the investment horizon matches the target date. As target maturity

funds invest in G-Secs, SDLs, and PSU bonds, the default risk is very low.

Investors can continue to hold their investments in short (including money market) duration funds as we expect a limited impact on these funds for a given

change in interest rates. An investor invested in a long-duration fund can exit their holding after considering exit load and tax event.